Term vs Whole Life Insurance: The Costly Mistake Millions of Adults Make

What if one financial decision today could save your family from financial hardship tomorrow?

Choosing life insurance isn't just another financial task—it's one of the most important decisions you'll ever make. Yet millions of adults buy the wrong policy because they don't fully understand the difference between term life insurance and whole life insurance.

The result? Some people pay thousands more than necessary, while others discover too late that their coverage doesn't meet their family's needs.

In this guide, you'll learn exactly how term and whole life insurance compare, who each policy is designed for, the hidden truths insurance companies rarely emphasize, and how to choose the right protection for your financial future.

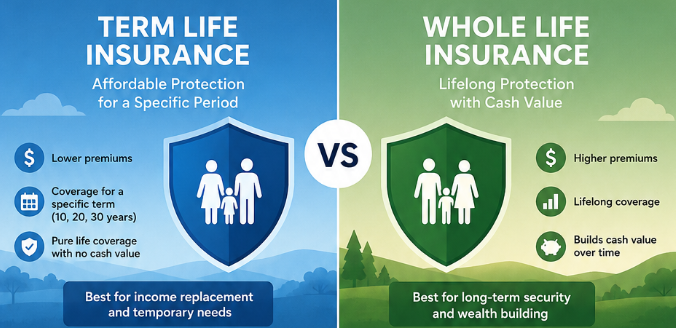

What Is Term Life Insurance?

Term life insurance provides financial protection for a fixed period, usually 10, 20, or 30 years. If the insured person passes away during that time, beneficiaries receive the death benefit. Once the policy expires, coverage ends unless it's renewed or converted.

Advantages

- Much lower monthly premiums

- High coverage amounts at affordable prices

- Simple policy structure

- Ideal for protecting your family during working years

- Excellent for mortgage and income protection

Disadvantages

- No cash value accumulation

- Coverage expires after the selected term

- Renewal costs may increase significantly with age

What Is Whole Life Insurance?

Whole life insurance is permanent coverage designed to last your entire lifetime as long as premiums are paid. Unlike term insurance, it also builds cash value over time, which may be borrowed against depending on your policy.

Advantages

- Lifetime coverage

- Guaranteed death benefit

- Builds cash value

- Fixed premiums that don't increase because of age

- Useful for estate planning and long-term wealth transfer

Disadvantages

- Significantly higher premiums

- More complicated than term insurance

- Cash value growth may underperform other investment options

Term vs Whole Life Insurance: Direct Comparison

| Feature | Term Life | Whole Life |

|---|---|---|

| Coverage Duration | 10–30 Years | Lifetime |

| Monthly Premium | Lower | Higher |

| Cash Value | ❌ No | ✅ Yes |

| Investment Component | No | Cash Value |

| Best For | Families & Temporary Financial Needs | Long-Term Protection & Estate Planning |

| Affordability | ⭐⭐⭐⭐⭐ | ⭐⭐ |

Who Should Choose Term Life Insurance?

Term life insurance is often the best option if you:

- Have young children

- Recently purchased a home

- Want maximum coverage at the lowest cost

- Need to replace your income for your family

- Are paying off loans or other major debts

Who Should Choose Whole Life Insurance?

Whole life insurance may be a better fit if you:

- Need lifelong financial protection

- Want to build cash value over time

- Are focused on estate planning

- Have already built emergency savings and retirement investments

- Prefer predictable premiums for life

"The best insurance policy isn't the one with the highest premium—it's the one that protects your loved ones while fitting comfortably into your financial plan."

Hidden Truths Insurance Companies Rarely Tell You

1. Most Families Don't Need Lifetime Coverage

Once your children become financially independent and your mortgage is paid off, your insurance needs often decrease significantly.

2. Expensive Doesn't Mean Better

Many people assume whole life insurance is automatically superior because it costs more. In reality, the best choice depends on your financial goals—not the price tag.

3. Buying Young Saves Thousands

Life insurance premiums are largely based on age and health. Purchasing coverage early can lock in substantially lower premiums.

4. Always Compare Quotes

Premiums can vary significantly between insurers for similar coverage. Comparing multiple providers before buying can save a considerable amount over the life of a policy.

Final Verdict

If your priority is affordable protection for your family, term life insurance is often the smarter option. If you're looking for permanent coverage, guaranteed benefits, and cash value accumulation, whole life insurance may better align with your long-term financial goals.

There is no one-size-fits-all solution. The right policy depends on your age, income, family responsibilities, financial objectives, and overall budget.

Plan Your Financial Future Today

Life insurance is only one piece of a strong financial plan. Before taking out a loan, buying a home, or financing a major purchase, it's important to understand exactly what your monthly payments will be.

🧮 Try Our Free Loan EMI Calculator →

Our free Loan EMI Calculator helps you estimate monthly payments, total interest, and the total repayment amount in just a few seconds. Compare different loan amounts, interest rates, and repayment periods to make informed financial decisions with confidence.